Negotiating Multiple Gateway Rule 11 Moves

Negotiating Multiple Gateway Rule 11 Rates for Movements

Imagine you’re in the market for a brand new [insert large ticket item]. You think you have a good idea of the price range, but how do you know for sure? Next, you shop around to compare prices, availability, included perks, and interest rates. All these factors are critical elements to be considered before making your purchase. Sounds logical, right?

If you were to replace the “large ticket item” with “Rail Rates,” does the same premise hold true? It should! Especially considering the monopolistic power that railroads have over rail shippers and their rates.

It is always good to get more pricing options from railroads. One of the best ways of doing this is to use Request for Proposals (RFP’s) that have railroads provide Rule 11 rates through multiple gateways. I know what you’re thinking: is the juice worth the squeeze? Is the potential savings enough to justify the time and effort needed to generate these RFPs and analyze the responses? Let alone rearrange the segments to complete the move? What if this was easy to do? What if the RFP and bid evaluation process could be done in less time? Then there would be no reason for NOT generating multiple gateway RFP’s. This type of RFP and bid evaluation process can be a game changer for shippers looking to reduce rail expenses. The barriers for doing this have been eliminated by the Rail Cost Control (RCC) program.

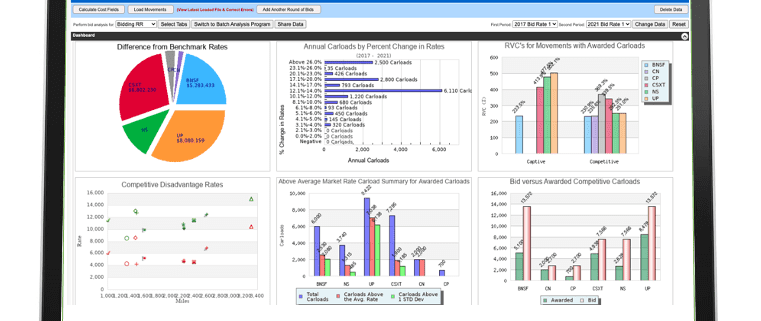

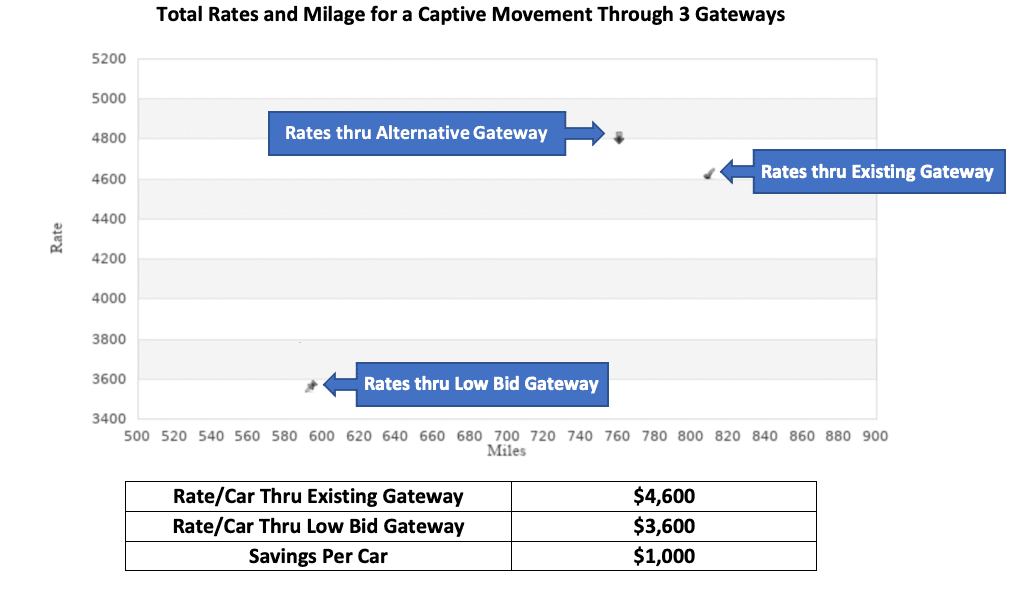

The illustration below provides a real-world example of the potential savings that can be generated for a captive movement by having railroads provide Rules 11 rates through multiple gateways. The total rate and mileage for this complete movement, through three different gateways, is shown below.

Mileage for the move ranges between 600 and 800 miles. The total rate using the existing gateway is $4,600, while the rate through the low bid gateway is $3,600.

The difference between the rate through the existing gateway and the low bid gateway is $1000. This move is for 50 annual carloads, which represents a savings of $50,000 on this one move. The low bid move also travels a shorter distance [200 miles shorter] thus improving transit times. Applying the full effect of this process on all of a shipper’s moves can easily add up to millions of dollars saved.

If you don’t go out to your railroads with multiple-gateway RFPs, how do you know you are truly getting the best rates possible? However, there is a harsh reality to generating Rule 11 RFPs for multiple gateways … Shippers can’t generate, analyze, and optimize multi-gateway Rule 11 RFPs for ALL their movements in excel.

To generate and evaluate multiple-gateway Rule 11 rates you’ll need a robust program that automatically does the work for you. This is exactly what the RCC – Cost Optimizer program does for rail shippers.

This comprehensive program allows shippers to AUTOMATICALLY generate multiple-gateway Rule 11 RFPs for ALL their railroads, for ALL their movements. Then RCC analyzes, optimizes, and even generates counterproposals the very same day responses are received from the railroads. Too good to be true? It’s not!

The Cost Optimizer generates RFP’s, evaluates railroad responses, determines win/win opportunities for both the shipper and railroads, creates counter proposals, and tabulates savings for management. The Optimizer is a finely tuned program that seeks out and quantifies your best opportunities for reducing the cost of rail freight.

Generating multiple-gateway Rule 11 RFPs is just one of many functions that the RCC provides rail shippers. If you’d like to expand your rate options, reduce your rail spend, and obtain immediate access to all your current and historical rates with just one click, schedule a RCC demonstration.

There is a better way to deal more effectively with railroads in less time.

See for yourself! Click this link to schedule a demonstration of the RCC program today.

Registration is still available for the 2022 Rail Negotiation Seminar. Treat yourself and your team to the #1 recommended rail negotiation program in warm & sunny Tampa, Florida. Click the banner below for more information.